I live in the USA and I am concerned about the future. I created this blog to share my thoughts on the economy and anything else that might catch my attention.

This is the End and a New Beginning

-

I've been thinking about this for some time.

After 21 years of writing this blog almost daily, I've decided to stop

writing the daily updates on the blog.

...

Silver Deep Dive

-

Silver had a memorable year (+148%). Some of this can be explained by a

decline in the dollar. I decided to do some ML analysis to look for other

insights....

Another look a NVDA

-

I've looked at NVDA a couple times, in *August 2023 *and *January 2024*.

On Saturday 8/26/23 I said the action in NVDA stock looked like it was

topping....

I saw this live on CNBC this morning. I flipped on the TV and saw that he was up next. It was definitely worth watching. He accurately predicted the stock market bubble. He accurately predicted the housing bubble.

Using long term analysis, Professor Robert Shiller, macromarkets chief economist at Yale University and the co-creator of the S&P/Case-Shiller Home Price Index, told CNBC on Friday that the S&P 500 may reach 1430 by the year 2020.

So let's do some math on his guess.

The S&P 500 closed today at 1257. In 2020 he thinks it will be 1430.

That's a 14% increase and it will take 10 years to achieve it. That works out to 1.3% per year. Meanwhile, he's assuming 2% inflation in his guess. I guess any real gains must therefore come from thejuicy 1.78% dividends.

I've used the USGS to generate the data in black from 1900 to 2008 and the median value in blue. The current data point uses data from the Massachusetts Department of Transportation and Kitco.

That everyone believes gold and silver have no downside makes me skeptical. If you are a buy-and-forget investor in precious metals, fine, but the market likes to destroy some wealth when the trade gets lopsided. The time to buy anything, gold and silver included, is after everyone who believed there was no possible downside has their head handed to them on a platter.

It's a good read for contrarians. He manages to cover many of the bases (from the recovery to China to central bank sure things). I prefer I-Bonds (and TIPS) over cash long-term, but that's mostly just a personal preference.

You will also note that I continue to lean deflationary in the short-term as seen in the upper left hand corner of my blog. That doesn't mean I think it is sure to happen. I simply believe that it is more likely than most seem to think, especially if Jim Chanos is right about China.

2011 could be a challenging year for cement manufacturers. Though demand for cement will reach higher double-digit growth, it will be insufficient to absorb the entire supply. Rising input prices and excess capacity (and resultant pricing pressures) will continue to depress margins for cement manufacturers.

In China investors bet money on cement companies after word spread that the government plans to build 10 million low-cost apartments over the next year. That's 72% more than the number constructed this year, according to Xinhua, and that means more of those slab buildings emerging from shrouds of bamboo scaffolding in many Chinese cities. Today Fujian Cement and Jiangxi Wannianqing Cement both hit the 10% daily limit.

Just keep betting money right to the end. You've got to handy it to thosesavvyChinese.

The Fed is, however, creating a new liability: the monetary base it creates to buy these bonds. In effect, it’s printing $1 trillion of money, and using those funds to buy bonds. Is this inflationary? We hope so! The whole reason for quantitative easing is that normal monetary expansion, printing money to buy short-term debt, has no traction thanks to near-zero rates. Gaining some traction — in effect, having some inflationary effect — is what the policy is all about.

The issue of commodity prices is a curious one; I’m getting a lot of correspondence along the lines of, “Well, which is it? Is it too much money printing, or is it greed?” But why does it have to be either of these? Why can’t it just be supply and demand?

Here's a summary of his opinions as seen above.

1. Quantitative easing will create inflation. 2. Quantitative easing does not lead to higher commodity prices.

You'd think that would be enough of ahecklefor one day but I'm not even remotely done yet. I refer you to his second link.

But I was and remain skeptical about the speculation story in 2007-2008, because of the lack of evidence of inventory accumulation;

I'm very disappointed that Krugman does not read my blog. Note the inventory accumulation in my extended pantry. I'm probably the only one in the entire world who is doing it though. *sarcasm*

There is currently $51.2 billion sitting inGLD. That's just one commodity fund of many. Would that be considered a speculation story? Is each and every investor planning to take delivery of the gold? Perhaps the thinking here is that investors will be creating jewelry for their significant others? If so, investors will be extremely disappointed. GLD has no intention of ever shipping the gold to its individual investors.

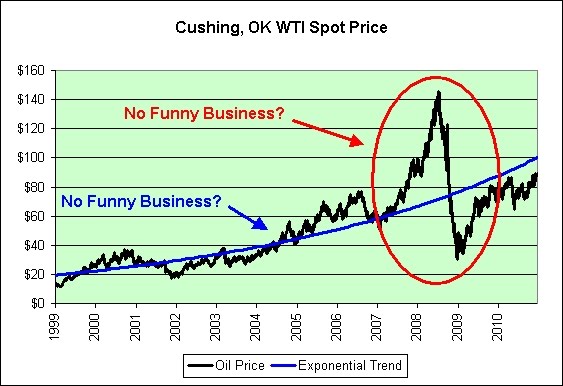

...and this time around, the fact that prices are still well below that previous peak suggests that there can’t be all that much funny business involved.

Let's look directly atoilfor any signs of funny business.

The circle in red "suggests that there can't be all that much funny business involved"? That's what Krugman claims. He also claims to be skeptical of the 2007-2008 speculation story. What would it take for him not to be skeptical of it? Would a pink elephant dressed in pink slippers screaming "I'm part of the speculation herd!" do it?

The line in blue apparently suggests that there can't be all that much funny business involved either. Oil will continue to double in price roughly every 5 years. How do I know that this trend will continue? Krugman tells me that "nobody believes in supply and demand". If true, everyone will continue to buy oil no matter how high its price goes. Nobody will even cut back. He's got a Nobel prize in economics. Who am I to argue? *sarcasm*

Krugman wants inflation. He claims quantitative easing will give us inflation. He's then surprised that anyone would think oil prices would rise based on quantitative easing? Perhaps he expected all that awesome inflation to magically appear in wages and housing prices instead? How else could anyone possibly explain his twisted logic?

Can't you just picture it. On a Friday afternoon the Fed announces that it WILL create enough monetary printing over the weekend to force up all prices by an average of 10%. Let's say Krugman is your boss. He calls you into his office. He says...

"I know your review isn't for 6 months, but based on what the Fed is doing today I have no choice but to give you a 10% raise immediately. I'm also sending you home early so that you can go to the mall and do a bit of shopping to help this economic recovery. You must promise me that you won't hoard though. The last thing this country needs is a panic at the grocery stores."

Let's all embrace Krugman's utopian dream. Although that is not how the real world works now, it could happen if we all wish hard enough. I'm sure of it!

This has created two side effects. First, investors have bought exposure to commodities as an economic hedge. Second, the price of foodstuffs has been bid up as low interest rates reduce the opportunity cost of hoarding them — especially in China, where the money supply grew almost 20 percent in 2010.

Psst! Don't tell Krugman these crazy economic theories! He'll think you are a nutcase.

America will continue to pump the financial system with liquidity via tax cuts and quantitative easing. China will keep the yuan cheap and avoid clamping down on inflation.

The tense equilibrium can't last for long, as either sovereign debt or inflation gets too heavy to bear. Whoever lasts longer, wins.

"Fraud!" cried the maddened thousands, and echo answered "Fraud!" But one scornful look from Casey and the audience was awed. They saw his face grow stern and cold, they saw his muscles strain, And they knew that Casey wouldn't let that ball go by again.

In December 2007, Rogers sold his mansion in New York City for about 16 million USD and moved to Singapore. Rogers claimed that he moved because now is a ground-breaking time for investment potential in Asian markets.

Precious metals could rally in 2011. They really could. It would be foolish to ignore 11 full years of solid backtesting.

2. Retailers

Retailers could rally in 2011. They really could. We didn't build all those American strip malls for nothin'. Don't let $90+ oil concern you. Load up!

3. Tech stocks

Tech stocks could rally in 2011. They really could. History clearly shows that you can never buy too many tech stocks. Which ones to buy though and in what ratio?

Apple: Valued at $43 for every man, woman, and child on this planet. Google: Valued at $28 for every man, woman, and child on this planet.

Decisions, decisions.

So there you have it. Precious metals, retailers, and tech stocks could rally in 2011. Now you know.

There's no mention of the worst that could happen in 2011. But what are the odds of that?

“Fundamentals are very bullish,” said Michael K. Smith, the president of T&K Futures & Options in Port St. Lucie, Florida. “There is optimism out there. China and India are growing. The demand picture will remain robust.”

When it worked to create the fund, one concern was that the exchange-traded product might contribute to a bubble. Burton and his investment team worried that too much success would shoot gold prices up too fast, resulting in a crash like the one that occurred in January 1980, he said. Back then the bubble burst in one day and took two decades to recover.

Pushing Every Button

Ultimately those engineering what would become SPDR Gold decided it wasn’t their job to worry about it.

“Our primary mission was to find every button we could push to stimulate demand,” Burton, 59, said in an interview in London. “We also knew that we had launched something that we could not control.”

...

“There was a potential perfect storm scenario where suddenly gold would fall into the clutches of hedge funds and momentum traders in very, very aggressive, leveraged plays, which could spike the price and then drop the floor out from underneath it,” Burton recalls of the talks.

“Our biggest concern was it would burn another generation of investors and you’d start the whole goddamned tale of tears over again,” he says.

Who is James Burton? He's the former CEO of the World Gold Council.

In July of 2010 I pulled this quote from the World Gold Council's website.

The World Gold Council’s mission is to stimulate and sustain the demand for gold and to create enduring value for its stakeholders.

I could not find that quote today but I could find this one.

The World Gold Council has a strong track record of delivering value for its members, its partners and broader society as a whole. The success of our programmes and activities is measured by their ability to maximise value for our members and our partners. As a result, value creation is at the forefront of all of our activities.

They've moved from "enduring value" to "value creation". How is one ounce of gold any different today than it was 10 years ago? It is the same gold is it not? Wasn't that supposed to be the allure? Gold's value is neither created nor destroyed? It's timeless?

We create value in a number of ways. Our authoritative research, insight and advice helps our stakeholders better understand gold and its role, both now and in the future. This authoritative position informs our innovations, allowing us to intervene in markets to create a step-change in the demand for gold.

Investors do seem to love financial "innovation" and market "intervention" paradigms. For example, our banking system certainly believed in "innovation" and "intervention" to "create value" for its shareholders. Right? How did that work out over the long-term?

In an ocean of propaganda, there are few forms of disinformation as annoying as the endless “gold bubble” babble.

Then prepare to be annoyed some more.

Despite the quintupling of the price of gold off of its absolute bottom, gold is arguably just as “cheap” today as it was when the price was below $300/oz. The reason is simple: the fiat paper currencies in which the price of gold must be expressed have been debauched/diluted by Western central banks (and the governments they represent) just as fast as the price of gold has been able to rise.

Who honestly believes that?

According toKitco.com, gold's absolute bottom was $252.80 on July 20, 1999. It now trades at $1,384.00. That's a 447.5% increase over 11.4 years. That works out to about 16.2% per year.

Meanwhile theseasonally adjusted CPI-Uhas risen from 166.700 (July 1999) to 219.146 (November 2010). That's an increase of 31.5% over 11.3 years. That works out to about 2.5% per year.

Gold has outperformed overall inflation by a whopping 13.7% per year and has done so for a full decade. And yet I'm told by "Bullion Bulls Canada" that a gold bubble is impossible?

Some might argue that the official government inflation figures are WAY off. Let's go down this path for a moment. Surely we'd see his "debauched/diluted" claim reflected in my electricity bill. We've been in an energy bull market for a full decade. Right?

So here's what my electricity bill has done.

The top rate for July 1999 was 6.8493 cents per KwH. The top rate for October 2010 was 10.3527 cents per KwH.

That's a 51.1% increase over 11.25 years. That works out to about 3.7% per year. It's a bit higher than the overall CPI-U but consider that I'm specifically picking an energy product here. I have not cherry picked deflating computer and TV prices in order to make my point.

Let’s assume that this 30% per year appreciation-rate is deemed “optimal” by these big-buyers. We can make a fairly persuasive argument that this is the case.

That passes for conservative these days? Even David Lereah wasn't *that* bold 10 years into a housing boom.

Update: I was off a year on my math. It was just over 11 years (not 10) and that's been corrected. I should have double checked my math before posting but at least I eventually got around to it. Sorry!

These findings further support the concern that the swelling ranks of elder Americans filing bankruptcy are simply running out of money. And when they do, the picture it is not pretty. For example, 9.7% report having gone without food while struggling before bankruptcy, 31.2% being late on rent or mortgage, 31.2% going without required medication (47.1% for the subset who filed for “medical reasons”), and 21.2% skipping doctors’ appointments (30.6% for the subset who filed for “medical reasons”).81 Thus, one of the most sobering findings of the CBP data may be this stark fact that although all bankrupt debtors are in tough financial straits, the elder filers are in really tough straits – an ominous portent of what may await the baby boomers.82 Whether this is related to the escalating costs of health care is certainly a possibility,83 just as is the prospect that the abolition of the defined-benefit pension plan is playing a role.84 It may also simply be the “financial shock” of retirement itself that elder Americans are ill-suited to face.85 (Recent data found credit counseling applicants citing “retirement” as a cause of financial distress among 5.4% of respondents; given only 9.4% of respondents categorized themselves as retired, this suggests that retirement has required pre-bankruptcy credit counseling for more than half of retirees.)86 Further exploration of these conjectures must await future study. The relevant observation for now is that credit cards may be a short-term (and ultimately unsuccessful) financing solution for the elder debtors to a structural financial deficit.87 If Americans cannot live out their senior years, even on Medicare, on their current incomes without relying on credit cards and then going bankrupt, we may be seeing early evidence of a deep societal problem of overindebtedness.

The chart shows the average annual Fed Funds rate over the previous 10 years (adjusted for inflation).

I would point out that we're pretty much back to 1979 levels and in hindsight that wasn't exactly the best time in recorded history to be embracing the commodity story long-term.

Here's something else we share in common with 1979.

Click to enlarge.

Note the similar steepness in the upward trend and the absolute level.

According to Kitco gold averaged $306.68 per ounce in 1979. It averaged $278.98 per ounce in 1999. It lost money in nominal terms over the 20 year period and much more in inflation adjusted terms.

Gold averaged roughly $1,223 in 2010 (still a few days left to go).

I suppose it could be argued that gold was a good store of value from a bubbly level in 1979 to the bubbly level now. It quadrupled while the CPI-U only tripled.

For those who are truly greedy 1980 was quite a year. Gold averaged $612.56 per ounce. It was the last part of the parabola. Gold doubled from 1979 levels. Maybe 2011 will be a similarly exciting year for gold? Who knows?

All I really know is that I have no interest in owning gold at these levels, especially when compared toaluminum. At $1,384.40 per ounce for gold and $1.0767 per pound for aluminum, the ratio between the two currently stands at a whopping 18,751 to 1. What must investors be thinking?

But the McDonald's menu has a unique problem that chemical companies and automakers don't have to deal with. It has a Dollar Menu, a list of items with a firm ceiling on price dictated by the very name that list carries. That leaves little relief to offset costs.

Which means one of two things could disappear in 2011: either the Dollar Menu moniker, or what’s left of McDonald's margins.

Here's what's left of McDonald's profit margins. As can be clearly seen, it's a tragedy of epic proportions.

It's a miracle that McDonald's can even stay in business with so few profits to distribute to its shareholders. How can any company survive when it earns just 20 cents for each dollar in revenue? We cannot expect McDonald's to absorb any further increases in costs. Those extra costs must clearly be passed on to its customers.

So take some extra time this holiday season to help McDonald's return its profit margins back to healthier levels. They need all the help we can give them. For the love of all that is holy, they are just shy of the profit margins over atCoach. Oh the humanity!

The recession has placed a terrible strainon the finances of the McDonald's investors. There has been too much violence. Too much pain. But I have an honorable compromise. If they remove the dollar menu, just walk away. Just walk away and there will be an end to the horror.

There has been too much violence. Too much pain. But I have an honorable compromise. Just walk away. Give me your pump, the oil, the gasoline, and the whole compound, and I'll spare your lives. Just walk away and we'll give you a safe passageway in the wastelands. Just walk away and there will be an end to the horror. - The Humungus, Mad Max 2: The Road Warrior (1981)

This week's AAII sentiment survey is out, and the bullish sentiment is out of this world: 63% bullish and only 16% bearish, for a bull-bear spread of 47%!

Wow!

The country is gutted, but meanwhile, we have another dotcom bubble complete with business model-lite companies, a farmland bubble, a precious metals bubble, and a generational bubble in ugly and degenerate art.

I'm not the only one who thinks there is "a precious metals bubble" apparently. That said, you might want to check out his source. Here's a freshlinkto it.

It would appear to be just some random crackpot doom and gloom blogger on the Internet. Everyone knows this is a period of untold prosperity and great riches though. You'd therefore be wise to be wary! ;)

In the chart above I'm taking Apple's historical stock price adjusted for splits and dividends as reported by Yahoo and I'm dividing by the apple inflation series (the actual cost of the fruit, 1982-84=100) as reported by the BLS.

Apple (stock) was a pretty good apple (fruit) hedge from 1985 to 2005. It then became much more than that.

For what it is worth, I'm not all that interested in hedging the future price of apples (fruit) by buying Apple (stock) at these prices. I suspect that the lowest lying fruit (stock) has already been picked from the Wall Street tree.

I hope this isn't too confusing. I'm basically suggesting that the $300 billion Apple stock is a bit fruity at these prices. That's over $43 for every man, woman, and child on this planet. I'll pass.

Here's the update to that chart. While updating the data I noticed that there have been some serious revisions to the data. It does not change the overall effect though.

I'm still bearish.

Apologies to all Darden investors. Perhaps I should have posted this chart sooner.

Stock tanks nearly 5% as Red Lobster and Olive Garden operator sees sales at existing outlets fall from last year.

In my defense, it was actually the news from Darden that inspired me to update these charts though. Go figure.

Here's a glimpse of gasoline sales.

Did I mention that I'm still bearish?

I offer a special thanks to Ben Bernanke. There's nothing quite like rising gasoline prices to create all kinds of pretend prosperity. Your ongoing actions should give this blog plenty of long-term staying power, lol. Sigh.

The following chart shows state and local financial assets vs. liabilities per capita and adjusted for inflation from 1959 to present. Note that over the long-term both have tended to grow.

Click to enlarge.

Note theretrograde motionin financial assets in recent years. This also occurred during our last consumer recession (as seen in the chart at roughly the $6,000 level).

It soon turned out that the quick recovery was illusory, and by 1990, economic malaise had returned with the beginning of the Gulf War and the resulting 1990 spike in the price of oil, which increased inflation but to less of a degree as the oil crisis ten years earlier.

The following chart shows the difference between the financial assets and liabilities.

Click to enlarge.

An optimist would say that we're now sitting very close to the median line in red. There's nothing much to see here. All is normal.

A pessimist would say that for the past decade we've been following the trend line in blue and that it is not sustainable long-term.

I'm somewhere between the two extremes but I do lean a bit more towards the pessimist argument. I would add that the illusion of prosperity we had in the 1990s has finally come back to haunt us. Note that all the net debt reduction that was done by state and local governments from 1993 to 2000 has been completely unwound.

That said, why should we even consider bailing out state and local governments right now? If adjusted for inflation and population growth, the net state and local debt is just half of what it was heading into the 1970s.

Sorry about that. There I go mentioning the 1970s again. Have no fear. I'm still leaning deflationary though. Why? Here's one reason.

We woke up in a Rentership Society, and it’s starting to look permanent. And you know what? Thank goodness. Ownership, it turns out, is for suckers.

Since I am retired, my car sits mostly unused in my garage. I picture myself someday using aZipcar instead. I just need a few to appear near where I live.

I'm also tempted to buy aKindleif only to comfortably read up to 3 million free online books. No hurry on that purchase though. The Kindle just keeps getting better and cheaper.

Now picture a wave of baby boomers just like me attempting to do the same. That's amazingly deflationary.

HAMMOND, Ind. — Former East Chicago Mayor Robert Pastrick has filed for bankruptcy, at least temporarily blocking state efforts to collect a $108 million judgment for racketeering.

A statistics expert in China who asked not to be named told Beijing Business Today that the reason for such a big discrepancy in CASS’s two predictions is that there is no uniform standard for scientific computation. They were based on an evaluation of the current policy and economic environment, but lack the support of basic research data.

Shocking!

You might think I'm shocked at the lack of a uniform standard for scientific computation or the lack of support of basic research data. That's not it.

I'm actually shocked that a statistics expert in China would ask not to be named. Shocked I tell you! Shocked!

Cao believes that China’s real estate bubble will burst, and its timing depends on the critical point of the overall Chinese economy. Once that point is reached, it will trigger a massive burst of the housing bubble.

Shocking? Not really. I've been desensitized, lol. Sigh.

If Sakakibara is right, the global economy is in deep trouble. He envisions a broad slowdown that might drag on for seven to eight years. China can live a couple of years without U.S. and European growth, but eight?

Gold in a depression. Gold has a particular status. To some people it is a thing, a commodity which rises and falls in price according to the play of supply and demand, just as soybeans and copper do. But other people see gold as money. And not just as any money but as the best of money. This latter way of thinking about gold makes the value rise during depressions.

I should probably point out that this article was written on September 22, 1979. In hindsight, there were clearly better times to be buying gold.

The investment will seek to replicate, net of expenses, twice the performance of gold bullion as measured by the U.S. Dollar p.m. fixing price for delivery in London.

The investment will seek to replicate, net of expenses, twice the performance of silver bullion as measured by the U.S. Dollar fixing price for delivery in London.

Early on, grocery stores were a common type of anchor store, since they are visited often. However, research on consumer behavior revealed that most trips to the grocery store did not result in visits to surrounding shops. As of 2005, the declining popularity of old-line department stores makes it necessary for mall management companies to consider re-anchoring with other retail alternatives, or mix commercial development with residential development to guarantee a captive clientèle. The challenges faced by the traditional large department stores have led to a resurgence in the use of supermarkets as anchors.

Missing from the chart is the $2.8 trillion in debt we've racked up in the municipal bond market. That's another $9,000 per capita that we owe. Have no fear though. We're told not to worry.

Armageddon makes for a sexy story. Volatility in the $2.8 trillion U.S. municipal bond market is real, but the scary tale being spun out of budget-busting states like California involves a lot of literary license.

There's nothing sexier than Armageddon. Agreed.

Yet while a state default isn’t impossible, comparisons with, say, Greece or Italy are misleading. California’s debt-to-gross state product ratio is just 5 percent — minuscule compared with the Greek debt-to-GDP level of 133 percent, as estimated for the year-end by JPMorgan, or the U.S. federal government’s 88 percent.

That's a fascinating way to look at it. I was under the impression that Californians owe money at BOTH the state level and at the national level. The least misleading way to look at it would therefore be to add the 5% state debt to 88% national debt and realize that 93% is not "minuscule".

It might also be worth mentioning that unlike the federal government, California currently does not have a monetary printing press. I don't think it takes "a lot of literary license" to therefore suggest that California really could run out of money someday.

The commodities that would be most adversely affected by the bursting of the China bubble and the consequent reduction in Chinese commodity consumption are the industrial metals. Oil also looks vulnerable to us, but uranium does not because we expect that China's plans to increase its nuclear power generation capacity will remain in place almost regardless of what happens in the real estate market. We doubt that gold would be adversely affected beyond short-term knee-jerk reactions, because gold is mostly held for wealth-preservation purposes and therefore tends to fare relatively well when economic problems abound.

1. Wealth-preservation implies that gold is neither gaining purchasing power nor losing it. However, gold buys a heck of a lot more toilet paper at Costco than it did 10 years ago. It also buys a heck of a lot more real estate. That's not wealth-preservation. That's get rich quick.

2. How much wealth did gold preserve between 1980 and 2000? As seen in thehistorical gold pricesand theconsumer price index, less than 25%. That assumes you didn't buy it at the very peak in 1980 of course. That would have lowered gold's ability to preserve wealth to just 15% over the period. Almost anything would have preserved more wealth than that, evensalt.

3. Since silver is thought to be partly an industrial metal and partly a precious metal, how much might we expect to see silver fall in sympathy? If silver falls in sympathy, what's likely to happen to gold?

4.Gold and silverwere extremely expensive compared to base metals back in October. Just how much higher do investors think they will go if base metals crash?

5. If industrial metals and oil are part of the China bubble story then why would I need gold and silver to preserve my wealth? Cash would seem more than adequate when the bubble eventually pops.

I would absolutely agree that a "greater fool theory" is being put into practice on a phenomenal scale. At least you could live in housing during the housing bubble. You can't even live in gold though. Its only value for "wealth-preservation purposes" is what someone else will pay you for it.

If you are a gold investor, then deep down you secretly hope that you will find someone else much more foolish than you when you decide to sell. It's the absolute truth. The more foolish the better. Been there, done that.

My girlfriend and I saw thisJoss Whedonvideo on Netflix recently. Netflix said she would rate it 5 stars. She did! It was extremely enjoyable. I present it in its entirety. I hope you enjoy it as much as we did.

Can you spot the egregious fiscal errors in his example of what the family ought to do?

There's so much debt, since we bought our tent That we camp every night We try to do it up right, but we just can't afford light We're not very bright

We got no cash and we beg for our food It's for our childrens' sake They bathe in the lake, there's so much at stake Our debt still keeps us awake

We camp in the heart of tent city Our house is empty and dark It was foreclosed and it's not pretty Our payments were just too far apart

Some of the bankers were friendly Some visit us even when they're not There's nothing left that can be stolen And we enjoy doing without

Heating our tent without an energy source Is just part of the fun We're under the sun, then cold has begun I sure wish we weren't shunned

The credit card bill is still making us ill But we almost drowned Rates were floating around, our massive debt was unwound As the whole thing crashed down

He's trying to get back to college But loans are a bit of a drag We thought they had a place and a purpose But bank lending has run into a snag

We once owned cars and a pickup It made finding jobs easy to seek Walking is now our new habit The world must be ours since we're so meek

So Disneyland's out, our future's soldout Our debt was our blight The sight is a fright, and so is hindsight Our day's turned to night

It's this fiscal mess that's put terrible stress On our nation's labor force There's been shutting of doors, no job offers of course And debt is the source

And it's par for the coarse to see that camping's endorsed As our jobs are outsourced

Plus, stock prices sometimes plunge. That's why retirees who buy stocks for income should probably limit their exposure to this strategy and stick with large, very stable companies with a history of paying dividends.

Here's a tip. ThinkCitigroup back in 2007. Stable? It was way too big to fail. Don't forget the decades of rich dividend payinghistory it had back then either. That just shows the power of the rear view mirror. There's all kinds of fun things to see.

Life insurance really isn't meant to be a retirement plan, but it can be a welcome additional income source for retirees who find they're a bit short each month. The safest policy for the job is one like whole life or universal life that builds cash value on a schedule.

When it comes to generating income, there's nothing safer or more reliable. While this strategy obviously isn't viable when CDs and savings accounts pay 2%, 1% or even less, it can be a fine option when interest rates are reasonable.

Obviously. You can't be earning 2% safely and reliably when inflation is just 1.2%. Wait for inflation to hit 3.2%. That way you can earn 4% instead. It might feel the same in some ways, but the extra taxes you pay on those inflationary profits will make all the difference.

And since you clearly cannot own CDs and savings accounts right now even though inflation is so low, that leaves you with only one obvious conclusion. You must chase returns elsewhere just like everyone else. Perhaps something that has skyrocketed in price over the past few years? Oil? Gold? Silver? Stocks? With so many obvious choices to choose from, how could you possibly lose?

Working part-time can be a good way to do that while earning extra income. And the only thing at risk is some time.

Time spent looking for work in retirement is time well spent. That's especially true when unemployment is 9.8% andage discriminationis prohibited.

Also keep in mind that gasoline is roughly $3 per gallon. The IRS believes it costs you51 cents per mileto operate a vehicle. That means you'll want to find a high paying part time job very close to where you live of course.

As an example, if you are earning $7.25 per hour (minimum wage), keep roughly $6 after taxes, you work 2 hours per day, and you accept a job that's 12 miles from your home, then you can expect to net $0. It won't feel like it at first, but it will when your car eventually needs maintenance.

I should probably stop here but I will leave you with a sarcastic haiku.

Financially safe And yetTIPSare not offered Snowball's chance in hell

"The U.S. has never spent Christmas with a $3-a-gallon average price for fuel," Oil Price Information Service said. The national average now is the highest since October, 2008, according to OPIS, and if oil prices linger near $90 a barrel, it could reach $3 before the end of the year, several analysts say.

"We're within spitting distance right now," said Stephen Schork, an energy analyst and publisher of The Schork Report. "Whether we get there by the end of the year or by the end of January, as far as consumer's concerned, we're there already by a psychological standpoint."

For what it is worth, gasoline pricescrashedin 2008. What was $4 in July and $3 in October was just $1.61 during that Christmas week.

Apologies to my European readers for mentioning $3 gasoline.

LONDON — Even as American drivers complain about "gas pains," they can count their blessings that they don't live in Europe, where motorists pay more than twice as much at the petrolpumps.

Here's a thought. What if you had to pay $3 a gallon for gas but were making just $1 per hour in a Chinese factory? Then what?

If there is a hard-landing in 2011, China’s reserves of $2.6 trillion – or over $3 trillion if counted fully – will not help much. Professor Michael Pettis from Beijing University says the money cannot be used internally in the economy.

While this fund does offer China external protection, Mr Pettis notes wryly that the only other times in the last century when one country accumulated reserves equal to 5pc to 6pc of global GDP was US in the 1920s, and Japan in the 1980s. We know how both episodes ended.

Employment growth among retail salespersons reflects rising retail sales stemming from a growing population.

...

Growth will be fastest in general merchandise stores, many of which sell a wide assortment of goods at low prices.

...

Despite the growing popularity of electronic commerce, the impact of online shopping on the employment of retail salespersons is expected to be minimal. Internet sales have not decreased the need for retail salespersons.

1. The government is predicting that 374,700 new retail salesperson jobs will be created between 2008 and 2018.

2. The government predicted that 565,000 new retail salesperson jobs would be created between 1998 and 2008.

3. Hindsight shows that 92,800 retail salesperson jobs wereeliminatedbetween 1998 to 2008.

4. The government continues to believe that online sales will not decrease the need for retail salespersons.

5. The government continues to see theoretical "employment growth among retail salespersons" thanks to a "growing population" and growth in stores selling "goods at low prices".

6. Stores that sell "goods at low prices" generally pay low wages.

Note the lag between the gasoline price shocks (peaks) and the shocks to employment (troughs). Also note the ruthless efficiencyof the continuous 2004 to 2008 gasoline shock (the part within the blue circle) to help create all kinds of employment problems (and temporary stock market euphoria). Isn't easy money wonderful? Wow!

The next chart shows what the previous two years of gasoline price movements generally do to the following two years of employment.

Click to enlarge.

The good news is that gasoline is cheaper than it was 2 years ago. In theory, we should see at least somejob creationbegin to appear. That's assuming we can think up some new labor intensive industries on a planet with 6.8 billion people of course (while simultaneouslyautomating service jobsand outsourcing our manufacturing base overseas).

The bad news is that the Federal Reserve seems determined to drive up the price of gasoline again. What if the "credible threat" of higher gasoline prices is all it takes to stop job creation?

Click to enlarge.

Note that this peak in the unemployment rate is not at all like the previous peaks. We're apparently attempting to construct a plateau.

By increasing the number of U.S. dollars in circulation, or even by credibly threatening to do so...

You can lead a horse to water. You can even credibly threaten him to drink. Can you actually make him drink though? The proverb says no. Horses apparently love unintended consequences.

Adjusted for inflation since 1980, silver prices should be trading at roughly $128 an ounce.

Should be? Seriously? Silver was one of the biggest bubbles of the past century back in 1980. It's like saying that the Nasdaq should currently be trading at 6500 in inflation adjusted dollars. Good luck on that one.

There's nothing quite like cherry picking the starting point in order to sway your audience though. The peak may have been $128 an ounce in 1980 (I can't say), but the average price for silver that year was an inflation adjusted $55.

Other than a silver bug, who really thinks silver will go back to that inflation adjusted high? It would be interesting to see how many trigger fingers would hover over the "sell" button just before it though, assuming it could even get that close.

If the plan is to be overly optimistic, then why not go all the way? Silver peaked at an inflation adjusted $1,081 per ounce in 1477. I'm using the $806 all time high as seen in 1998 dollars and then converting those dollars to 2010 dollars.

Please note the 99.3% loss in purchasing power from 1477 ($806 per ounce) to 1998 ($5.55 per ounce). That's the kind of thing I thought about when I owned silver from 2004 to 2006. I had many, many concerns. Modern mining equipment? Mr. Fusion? Not once did I think my silver investment was a sure thing.

Remember this tip, though – one that goes for any investment: When everyone is talking about a sure thing, be skeptical and diversify. For example, Abu Dhabi’s Emirates Palace Hotel recently opened a vending machine that dispenses gold bars! Choose your investments carefully and be sure to distribute your capital into other hedges like cash, silver and oil.

That's considered diversifying? You add two other "sure things" to your one "sure thing" and then park the rest in cash?

Let's say you retired in 1980. That's the date we're told to concentrate on. Had you "diversified" your nest egg by burying gold, cash, silver, and oil in your backyard at that time, then you could have been financially ruined over the following 20 years. Not one of those four things kept up with inflation. Not even close. As seen in the chart below, the ride down in silver would have been especially brutal.

Click to enlarge.

Note that silver is now nearly 4x more expensive than its long-term inflation adjusted median price (using annual data from 1913 to 2008). I opted to use the median price instead of the average price to better take into account the 1980 bubble. Medians do a good job of stripping out spikes in the data. I think you can see that in the chart. The red line is a reasonably good fit.

In my opinion, silver is now in crazy tin foil hat territory. I have no idea how long it can stay there or how much higher it can/will go but I can say this. I am a believer in a return to the mean/median someday.

This does not necessarily mean I think that inflation will remain tame. I'm simply saying that there is serious risk that silver will not keep up with inflation long-term if bought at these levels. If one must buy silver at these prices, then at least consider hoarding some toilet paper to go with it. Toilet paper hasn't been bid up by speculators with potentially itchy trigger fingers and get rich quick hopes and dreams. As a hoarder of toilet paper, I can say that with 100% certainty.

It is certainly possible that the world is running out of energy, oil, gold, silver, copper, and so on, and so on. It is also quite possible that the Fed is blowing bubbles again. I think you can guess where I stand on that. They wanted us to take on more risk in order to prop up prices again. I'll pass. It just never seems to end all that well. The popping of each bubble is a complete surprise of course. Few ever seem to see it coming.

And lastly, I'm told to be excited about the stock market again and how fantastic our recovery is going (as seen on CNBC). However, I will repeat what I've been saying since the beginning. I am not a believer in commodity driven stock markets. Show me a stock market that is rising without oil rising someday and then perhaps I will be interested. Oh please let it be Mr. Fusion. Now that would be something to cheer about.