I live in the USA and I am concerned about the future. I created this blog to share my thoughts on the economy and anything else that might catch my attention.

This is the End and a New Beginning

-

I've been thinking about this for some time.

After 21 years of writing this blog almost daily, I've decided to stop

writing the daily updates on the blog.

...

Silver Deep Dive

-

Silver had a memorable year (+148%). Some of this can be explained by a

decline in the dollar. I decided to do some ML analysis to look for other

insights....

Another look a NVDA

-

I've looked at NVDA a couple times, in *August 2023 *and *January 2024*.

On Saturday 8/26/23 I said the action in NVDA stock looked like it was

topping....

CAIRO (AP) -- Fitch Rating on Friday revised down its outlook for Egypt, dropping it to "negative" as mass protests in the country turned violent, engulfing the capital and other cities in a serious challenge to President Hosni Mubarak's 30-year rule.

You've really got to hand it to the analysts over at Fitch for spotting thetanks in the rear view mirror. This will no doubt help all the investors who don't have access to global news but yet still somehow have access to Fitch.

This isn't the first time Fitch has helped investors though.

Fitch "believes that AIG is likely to pursue other steps to raise cash and capital and that the company may pursue the sale of various operating units." It adds in its statement, however, that "these measures will take time to develop and thus while they are likely to provide AIG with long-term benefits, they are unlikely to provide benefits in the short-term. Notwithstanding Fitch believes the accommodations being provided by AIG's insurance regulators has eased the potential liquidity strain being experienced at the holding company level."

Unfortunately, Fitch did not factor Fitch into its analysis.

“Japan has the worst generational inequality in the world,” said Manabu Shimasawa, a professor of social policy at Akita University who has written extensively on such inequalities. “Japan has lost its vitality because the older generations don’t step aside, allowing the young generations a chance to take new challenges and grow.”

Click to enlarge.

I had no idea that the younger workers of Japan had it so bad. As seen in the chart above, it is roughly half as bad as it is for the younger workers in America.

We do not want to end up like Japan. I must therefore beg older workers to step aside. Please. Do it for the children.

We've only had one decade of extremely poor stock market performance. Japan has had two. See? Our situation isn't even remotely the same. If you are an older worker, there's absolutely no reason to keep working.

“In France, the young people take to the streets,” Mr. Takahashi said. “In Japan, they just don’t pay.”

The young people in France take to the streets? Let's add that to the chart. Maybe there's some sort of clue to be found there.

Click to enlarge.

As a side note, if you happen to have a 40-year-old unemployed girlfriend who is back in college in an attempt to compete more effectively with the younger workers of the future, then welcome to the club. We aren't even Japanese. Yet.

I have added an exponential trend line. I think it is appropriate here because there really is a finite supply of farmland in Montana. Over time we would therefore expect to see the value of farmland rise faster than inflation overall. In this case, the trend shown in red has been a reasonable 1.4% over inflation (as reported by the government in the CPI).

This most recent bubble is very impressive. Just look at the steepness of the ascent. Wow. That said, perhaps most of the damage is done. 2010 prices were unchanged from 2009. Those who hold this farmland over the long-term and can actually make productive use of it should do okay in my opinion. Know that you would be likely be paying a premium though.

The Federal Reserve System (also known as the Federal Reserve, and informally as The Fed) is the central banking system of the United States. It was created in 1913 with the enactment of the Federal Reserve Act, largely in response to a series of financial panics, particularly a severe panic in 1907.

Thank goodness we don't have any more financial panics. Mission accomplished!

We need to watch the land values and be prudent but I do not think we need to be overly pessimistic there will be a crash in values. In 2009 land values dropped slightly. This shows there is still discipline in the market. There may be a speculative bubble that impacts land as an investment but for now land still remains a good investment.

I think that's a fairly balanced way to look at it. However, Iowa's prices have not corrected like Montana's prices have. It would therefore seem likely that there is more downside risk.

The article provides a decision tool to compare the economic and financial impacts of purchasing a parcel of farmland. You might want to check that out too.

Years ago, I stopped driving around in search of better gasoline prices because the treks cost more money in wasted gas than they were worth.

Years from now he might even realize that the most expensive part of vehicle ownership is not the money spent on gasoline.

Car maintenance is something that should not be ignored. It is easy to spend 1 cent per mile just on the tires alone (assuming $400 tires with 40,000 miles of life).

There's also the increased risk that comes with driving more. There were 6.5 million auto accidents in this country in 2005 at a cost of$230 billion. That was roughly $1,150 perregistered driver. I won't mention the death every 12 minutes and disabling injuries every 14 seconds statistics. Oops. I did.

The IRS allows businesses to deduct50 cents per mile. They do not do it out of the goodness of their hearts. That's not even counting what a person's time is worth as they drive out of their way to find "cheaper" gasoline.

Thankfully, I did a little math before heading out.

Indeed. Very little math. None of this was factored in. Only the price of gasoline was deemed worthy for consideration.

The best journalists in the world work for The Times and there's no debating that.

As far as government deficits go, what we argue is that there are no financial constraints-there is a real resource constraint. In other words, inflation is the ultimate constraint. We shouldn't be constructing fiscal policy with some sort of vague, undefined notion that it's fiscally sustainable. Nor should we define "fiscal sustainability" via some arbitrary number as Kenneth Rogoff and Carmen Reinhart have done in their recent book, This Time Is Different: Eight Centuries of Financial Folly, wherein they say if a debt-to-GDP ratio gets above 90%, then bad things start to happen. That's not an accurate way to look at it because you have to consider the economic context and the institutional arrangements governing the economy. A pure fiat currency regime, as we have in the U.S. or Canada, for example, is vastly different than a country which operates a currency peg system, such as Latvia or Argentina in the 1990s.

I would tend to agree or I would not want to own TIPS.

MA: I don't think inflation per se is a problem. Food and energy price increases have been significant and they are real. I'm not trying to diminish their importance; but in the absence of income and job growth, people have to heat their homes, fuel their cars and feed their families. That just means more discretionary income is tied up in those areas, which means less discretionary income for retail, restaurants, etc. I think the ultimate impact is deflationary rather than inflationary.

Also, the high rates of unemployment are not going anywhere. Labor has no pricing power. There's no generalized increase of consumer price inflation. As that perception grows, the marginal bid could be taken out of the gold market for a while, which is why I am cautious on the gold price short term.

Once again, I would tend to agree. I'm just not seeing the increases in consumer price inflation that many seem to see.

The Kleenex boxes got smaller. What was once 300 sheets per box is now 260 sheets per box.

It cost $12.91 ($14.99 + 9.5% sales tax - $3.50 Costco coupon) in October.

It now costs $14.01 ($15.99 + 9.5% sales tax - $3.50 Costco coupon) in January.

I'm not quite done describing the situation though.

This is for the deflationists.

You now get 10 boxes instead of 8!

"New! LARGER PACK"

There's no mention that the boxes are smaller, lol.

So what does this really mean?

What once cost $12.91 for 2400 sheets now costs $14.01 for 2600 sheets. I checked the size of the sheets and they have not changed.

The increase in the price per sheet works out to 0.17%. Nice job Kimberly Clark. Way to hold the line. You manged to eek out a 0.17% increase, much like rates found on short-termTreasury Bills.

The battle between the deflationary forces of the Great Depression and the inflationary forces of the 1970s rages on.

That said, I do now have a 30% return on the investment in the garbage baghoard. Sugar prices are also way up (not seen in the picture). I'm not seeing much price action elsewhere though. Kleenex is the pillar of price stability. I could name off quite a few other items showing similar stability (from Ensure to spaghetti to sneakers Made in China).

For what it is worth, I'm just not seeing much inflation at Costco and I do continue to look.

As a side note, Kleenex is a staple around here. Not only do we have allergies but we also have one ofthese. I do not think it is possible to hoard too much of it, lol.

#1 Overbought (every Second you hear commercials to BUY GOLD)

I left the radio on and heard 86,400 commercials in one day. It worked out to exactly one per second. He's not exaggerating.

#2 Fear is disappearing (money moving to riskier assets)

I was under the impression that precious metals had become riskier assets at these prices. Apparently I was mistaken.

#3 As economy approves Government will raise interest rates

The economy will no doubt "approve" government just as much as I do, lol.

#4 As economy approve Government will remove all stimulus

Count on all stimulus being removed. Nothing left at all. A press release will announce that the country is fixed and there will be no further need of politicians. They will retire and flowers will be planted in their honor. Count on it.

#5 All you hear from politicians is to cut the deficit

That's all we hear. It's been true since the dawn of time itself. It is the one thing that both the Republicans and Democrats can agree on without reservation.

#6 Good news is bad news for the market,no more stimulus causing a correction in the market.

This will happen as the economy "approves" no doubt.

#7 Companies are reporting record earnings,hiring is just around the corner

If true, none of these new hires will use that money to buy silver apparently.

#8 As price goes down the main buyer of PM is ETFS they will keep unloading causing excess PM on the market

A falling price will lead to a falling price? Never saw that one coming. Genius!

#9 Dollar will rebound because of the strength in the economy

If we "remove all stimulus" and there is "strength in the economy" once we do that, then the dollar will surely rebound. I felt the need to summarize several of his ideas in the form of a disclaimer.

#10 At these lofty levels producers are waiting to buy at a better price for production.

Does this apply to silver producers?

I didn't really see much value in silver at these prices. However, if these truly are the top 10 reasons to short silver then sign me up. Shorting silver sounds like a "sure thing" to me. I certainly can't fault the logic any more than I already have.

Update:

Oh bummer. His post had 5 stars but has dropped to 4 stars in the time it took me to type this. I can't imagine why everyone didn't continue to "approve" of his reasoning.

(In all seriousness, I have no desire to own silver at these prices. It doesn't stop me from being an equal opportunity heckler though. The "economy approves government" quote was just too hard to pass up, lol.)

Here's a chart comparing the number of people employed in financial activities to the number employed in manufacturing, retail trade, and wholesale trade.

Here's where we will be in 80 more years if the exponential trend continues.

Now let's do the same thing with government employment.

Here's where we will be in 30 more years if the exponential trend continues.

And lastly, let's combine the two.

Here's where we will be in 5 more years if the trend continues.

In other words, in 2016 we could easily have as many people employed in government and financial activities as will be employed in manufacturing, retail trade, and wholesale trade.

Is it any wonder why our economy is struggling?

This post inspired byUK Bubbleand by the commentary foundhere.

In a widely expected decision, the Bank of Japan's nine-member policy board voted unanimously at a two-day meeting to keep the overnight call rate target at 0 to 0.1 percent.

The big difference is silver is spread out in many hands this time and I am sure the big players (Chinese, Hedge funds, etc.) have plenty of cash this time and will meet the margin calls.

1. Spreading the risk does not necessarily reduce the risk. This is especially true during bubbles.

2. If the big players had to resort to using margin loans to buy silver, then I would argue that they probably don't have plenty of cash.

Yesterday’s TIPS (Treasury Inflation Protected Securities) auction was lackluster, at best, with the lowest bid to cover ration (demand) in nearly two years.

Inflationary fears caused investors to not want "inflation protected" securities. Who knew? As a side note, I have never heard of a bid to cover "ration". It does sound like something I might hoard though.

The acrid smell of inflation is starting to spread around the world and likely is behind these rate increases as the “bond vigilantes” flex their muscles.

Something "likely" smells fishy.

As seenhere, yields on long-term treasuries without inflation protection rose much more than treasuries with inflation protection over the past week. That means treasuries with inflation protection were less desirable than treasuries without inflation protection. Just which muscles were the bond vigilantes intending to flex?

Perhaps the putrid smell of deflation is overwhelming the acrid smell of inflation over the long-term? It is a wonder the bond vigilantes have any sense of smell left at all. Perhaps they have packed their sinuses with bid to cover rations as a defense, lol.

"It is an industry that has always gone up," says Andrew Murstein, president of Medallion Financial. "It has outperformed every index you can think of — the Dow, Nasdaq, gold, you name it."

If it works for the taxi industry, then why can't we just apply it to the beef industry?

For Murstein, recent price surges are not surprising; medallions have seen an average 15%-a-year appreciation for 70 years, he says.

"Not only do you get that 15% for your price appreciation, you also get rental income," Murstein says.

I'm still working through the rental income part. Maybe we could apply that to dairy cattle. Got milk? No. Got milk medallions? Hell yes! And I got in early too! Woohoo!

Daus says the financing provided by Medallion Financial is key for many cabbies to make that transition to ownership, and that the company's mission seems to be "helping people achieve the American dream."

Former New York governor Mario Cuomo, who sits on Medallion Financial's board of directors, agrees.

Yes indeed! Taxi cab medallion financing sure "seems to be" helping people achieve the American dream. Who could afford to pay half a million dollars for just the right to drive a cab without the financing?

Here's the really good news though. I think it is safe to say that politicians would be all over my all beef prosperity creation idea. In fact, if you are a politician please contact me and I'll reserve a place for you on my board of directors. Vast riches for all of us. Win win!

I'm taking the annual growth in our national debt, adjusting it for inflation, and comparing it to the average unemployment rate over the previous 12 months. This data goes back to 1966 so it includes the dreaded 1970s. The blue dot shows where we were as of the end of the third quarter in 2010.

First off, I want to say that I find this chart encouraging. I wasn't sure what to expect when I was creating it. It is much better than I feared.

Although I am very bearish long-term, I realized that there are many people far more bearish than I am. I turned on the radio this evening and was immediately hit with the radio show host talking about hyperinflation in an ad and telling us how we can protect ourselves by buying gold. Good grief.

As seen in the chart, I think gold investors would be very disappointed buying at these levels if we can get the unemployment rate down to even 7%. It may take time, but I do think it is possible.

At 4% unemployment investors felt that 10% unemployment would never happen again. In fact, I debated bulls on the Yahoo's Capital One Financial message board about the perils of assuming that unemployment would stay low back in 2007.

So far COF's customers are paying their bills. However, with near record unemployment why would we think otherwise? What will happen if unemployment reverts to the mean?

(I was speaking of near record low unemployment at the time.)

At 10% unemployment investors feel that 4% unemployment will never happen again. Maybe that's true. Who knows? I can say that 7% is the mid point of the two extremes though.

I'm not suggesting that 7% would make it all biscuits and gravy, but it would put us within striking distance of at least some sustainability. Or at the very least, make it possible to push off our eventual day of reckoning to long after I am dead and buried.

Perhaps the gold bubble of the 1970s was not popped by rising interest rates. Maybe that's just an assumption. Perhaps it was falling unemployment that did it. Because let's face it, there would be far fewer bears if our national debt situation was sustainable and it would clearly be more sustainable if more people actually had jobs. I would also point out that I do think gold has been in a bubble (since crossing $1000) and have stated that opinion many times on this blog.

In summary, I am very bearish but I am not apocalypse bearish. I did not createthisbecause I was planning for the end days. I did it because real interest rates were so low and I couldn't think of anything better to do with the money. That's all. I'm not about to move to China for a better life. This is America and we still have a lot going for us if we can just get our act together.

But I see this as a time to batten down the hatches, buy your insurance and lock in your wealth and assets in terms of purchasing power.

I find it odd that he speaks of buying gold to lock in purchasing power when it is SO expensive comparedto the things you would someday purchase. For example, the miraculous metal known asaluminumisnowhere to be foundon his site. That said, I find many of the things he says to beodd. Apparently I am not the only one.

Why do people continue to give credibility to an operation like Shadowstats? Now that's something that I'd like to hear explained. - James Hamilton, September 4, 2008

The Mundell–Tobin effect suggests that nominal interest rates would rise less than one-for-one with inflation because in response to inflation the public would hold less in money balances and more in other assets, which would drive interest rates down.

I hadn't really given this much thought. I just sort of assumed that the Fed was the only one driving interest rates down if inflation picked up.

Think about it though.

1. You are 50% in stocks and 50% in cash. 2. The CPI starts climbing at 1% per month pace. 3. That cash position stinks.

So there you are. You've got a problem.

What do you do next?

1. You could buy something with that cash. 2. You could buy some bonds that pay at least some interest. Something is better than nothing.

If you choose option #1 then the person you bought from will be faced with the same problem you just had. Eventually someone will choose option #2. When they do they will be driving interest rates down.

So while it is true that bonds yields would rise as inflation rose, there would be some money that was once in cash that would move into bonds. It would therefore seem likely that nominal interest rates would not rise as fast as inflation rises. That's assuming I understand this process correctly.

1970s

UK RPI: ~13.7% UK Short-Term Rate: Ordinary Funds, Consistent Series: ~9.5% UK Real Interest Rate: ~-4.2%

US CPI: ~7.8% US Short-Term Rate: Ordinary Funds, Consistent Series: ~6.8% US Real Interest Rate: ~-1.0%

Wow. I thought real interest rates were bad in the US during the 1970s. I hadn't looked at the United Kingdom.

That's why I am so willing to lock in any kind of positive real interest rate long-term.

I have anecdotal evidence that supports the Mundell-Tobin Effect. My IRA sat in cash for more than 4 months because I did not think inflation would be much of an issue. Had inflation been running at a higher rate I would have kept that money in TIPS and therefore driven the TIPS real yields down.

It was “not a good auction at all,” said Richard Gilhooly, director of rates strategy at TD Securities. “This appears to be a sound rejection of the need for inflation protection.”

It was a good auction for me. It's not like I was rooting for a lower rate.

The 29-Year TIPS I bought earlier this week is being taken out behind the woodshed and old-yellered. I'm fine with that. As I said when I bought it, I'm holding until maturity anyway so it really doesn't matter to me what other people are willing to pay for it.

Further, I am still planning to make a major purchase in February's 30-Year TIPS auction outside of my IRA. Bring on the higher rates!

Heck, if this continues we might even see something better than a 0.0% rate on I-Bonds by the end of the year. Wouldn't that be something.

Higher rates? The market thinks inflation protection isn't needed? As a saver I am certainly not complaining.

My guess is that if you see a significant slowdown of Chinese economic growth, that will hurt the non-food commodities market a great deal. A lot of the commodities’ prices are held up by Chinese stockpiling and Chinese investment-led growth. I don’t think it will have such a negative effect on food commodity prices. It depends on how the rebalancing takes place in China.

Here's one of the more amusing quotes.

Japanese workers are eight to ten times more productive and expensive than Chinese, and to compare the levels of infrastructure just doesn’t make sense. It’s like saying, “Let’s go to Haiti and build a supersonic flight transportation from one end of the island to the other.”

And here's one more for good measure.

You seem far more optimistic about America’s ability to get its act together.

Deep down I guess I am too or I wouldn't have nearly my entire nest egg in inflation protected US debt. We could very well be the best of the worst.

If you look at the US in 1929, 1930 and 1931, it was a period when American arrogance was simply out of control. They believed that since they were a high savings, surplus country, they were in the catbird seat.

Jim Rogersmoved to Asia in2007so he could be in the catbird seat. Right?

This article was offered by Coba in the comments. His comment got stuck in Blogger's SPAM filter but I finally noticed it. D'oh!

In the early 1990s, when Japanese rates were generally at a higher level, a yield curve inversion signalled a period of oncoming economic weakness. However, since 1995 the BOJ target rate has never exceeded 0.5%, during this time Japan has entered 3 defined recessions, however the 2 year 10 year yield curve has not even come close to zero.

There's a nice chart of this on that blog. Japan has experienced an upwardly sloping yield curve (just like our current one) since their housing bubble burst roughly two decades ago.

I am not comparing the US economy to the Japanese economy, I am however pointing out that a prolonged period of low rates can reduce the ability of the 2 year 10 year curve to predict future economic activity.

I think this is a serious risk and I would like to once again bring up the chart Iposted yesterdaywith some visual enhancements on it.

Note that our 3 most recent downturns required an amazingly long period of extreme accommodative Fed policy (compared to previous downturns). Should this trend continue long-term we might actually end up in a situation where we require an infinitely long period of accommodative Fed policy someday. We might be in such a period right now. Who knows?

Is our economy truly self-sustaining right now? If the Fed announced that they would end their assistance of this economy right now and let the natural market forces take over then what would happen on Wall Street? My guess would be sheer panic. I'm talking biblical fire and brimstone level panic.

This post inspired by acommentleft for me on the TLT thread.

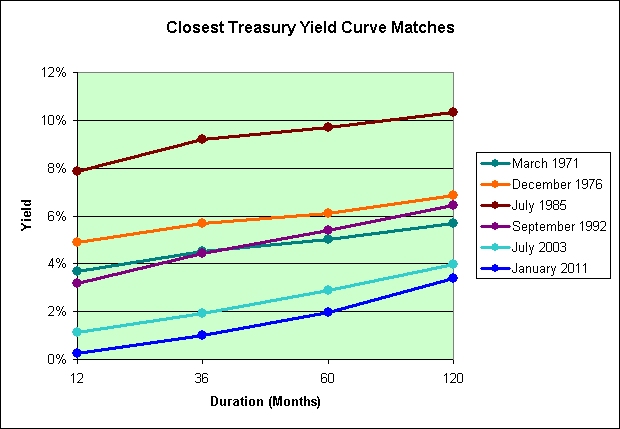

The following chart shows how well the current treasury yield curve matches yield curves of the past. I'm using the historical yields of the 1-year, 3-year, 5-year, and 10-year treasuries since that data went back the furthest. I'm just comparing the shapes, not the absolute values. Zero represents an exact match. (I'm summing up the squares of the differences so in theory it could go to infinity.)

Here's a chart of the closest matches. The blue line shows the current yields. Note the similarity in the shapes of the curves.

The following chart shows what the CPI might do over the next 3 years if all goes according to plan. The three most recent matches saw inflation rise by roughly 3% per year over the period. The 1970s saw more.

This last chart shows what interest rates might do over the next 3 years if all goes according to plan. The short end of the curve is where most of the action would likely be. In two of the five periods the yield on the 10-year treasury actually fell.

This assumes that all goes according to plan though. It might. It might not. I tend to think that we'll see smaller increases in the CPI and smaller increases in interest rates. This is mostly based on what I think might happen in China. Time will tell.

Remember, this is a military operation. Nothing ever goes according to plan. - Ludwig Beck, Valkyrie (2008)

I remain a reluctant short-term deflationist who has most of his net worth in inflation protected treasury bonds and inflation protected I-Bonds. That pretty much shows you my level of conviction. Over the long-term I expect to see higher inflation and/or slower growth.

It was. TIP now trades at 107.61. That's 29 cents in my favor. I lost 86 cents in distributions though. Sitting in cash therefore cost me 57 cents per share overall. That works out to about 1/2 of 1 percent.

Now for the good news. The 30-Year TIPS bond yielded1.59%on August 26, 2010. I was able to buy the 29 year TIPS bond today with a yield that was roughly 0.3% higher. Over the course of 30 years, that's about 9% more (0.3% x 29).

Although I lost some purchasing power on the move to cash, the ends justifies the means. I actually feel pretty lucky here. I was planning to wait until the 30-Year TIPS auction in February but this yield was just too tempting. I am very pleased with how this worked out.

97% of my IRA now sits in that one bond and I will be holding it until maturity. I do not want to be forced to ever sell this bond to someone else (a "greater fool" perhaps). I will therefore use the interest it generates over the years to buy TIPS that mature before my minimum required distributions kick in at age 70.

In theory, thanks to compound interest my IRA's purchasing power should grow by about 73% over the next 29 years.

1.019 ^ 29 = 1.73

I really don't care all that much what the market value of the bond does between now and then. The reason I don't care is that I don't intend to sell it to anyone else. I therefore don't care what others think it is worth. I know roughly what it is worth to me.

My IRA planning is now complete. I'm done.

As a side note, my IRA will never find its way back into the stock market. I will be rooting for the stock market though. The better this economy does the more likely that I will actually get paid. That said, I remain bearish long-term. I'm hardly swinging for the fences here.

If this one bond ultimately ends up being a losing trade for me, then I surely will not be alone. It will mean that the US defaulted on its debt and/or the currency completely fell apart. These are not trivial risks. I am simply trying to play the odds as I see them though. I am taking a risk here, but then again everyone is.

The financial policy of the welfare state requires that there be no way for the owners of wealth to protect themselves. - Alan Greenspan (1966)

Jan. 14 (Bloomberg) -- Federal Reserve policy makers may be relieved fuel costs at two-year highs are prompting consumers and investors to worry about rising prices, according to economists like Michael Feroli and Dean Maki.

Over the last decade we've worried about the September 11 attacks, several wars, the bursting of the dotcom bubble, the bursting of the housing bubble, our ongoing debt crisis, our ongoing trade deficits, and the ongoing surge in oil prices. The Fed has chosen to concentrate our fears mostly on that last one. This should come as a great relief to all of us.

“From the Fed’s perspective, strictly speaking, it’s good that year-ahead inflation expectations are increasing,” said Feroli, chief U.S. economist at JPMorgan Securities LLC in New York and a former Fed economist. “The point of maximum risk is most likely behind us,” he said, referring to the threat of deflation.

The point of maximum risk is behind us now. Rising fuel prices have saved us all. I think it pretty much goes without saying that a cheap energy source to fuel oururban sprawlwould be just too terrifying for words.

StockScouter compares the fundamental and technical qualities of stocks to measures that have proven statistically predictive of stock performance in the past.

I have similardevices installed in my car. I don't know where I would be without them.

If there is one"sure thing"we can count on, it is the predictive power of complex gambling systems.

Here's achartshowing the returns over the past few years.

This is great news for the"fringe pundits"who think the "exponential explosion" in the price of gold and silver will continue. Imagine all those future profits with so little risk?

And if you can't trust Morningstar to say it like it is, then who can you trust?

Do not assume that it is time to bail out, though. "The future may not be as bright, but we're not in a bubble mode," said Dan McNeela, an analyst with Morningstar. "Real estate is still a good diversifier."

Morningstar analyst Matt Nellans said AIG had shown that its margin of safety was great enough to survive everything but "the Great Depression."

Here's achartof AIG. Note its stock price in 2007. If we can believe Morningstar, then this must be "the Great Depression". Check out AIG's "margin of safety" as seen in the rear view mirror. How could anyone have seen this coming?

I wondered today how the market trades TIPS just before and after the auctions. Here's what I found.

The following chart shows the difference in yield in the trading days around the auction compared to the yield on the day of the auction.

Click to enlarge.

Note that the day of the auction tends to give you the best yield (as seen in the red line in the chart above). This is an assumption I have been working off of since becoming a TIPS investor back in 2000. In a perfect world, a truly efficient market wouldn't allow this to happen though. The extra supply on auction day would already be fully priced in.

The chart below shows how you would have done as an investor by participating in the auction vs. buying on a typical day near the auction.

Click to enlarge.

There is not much data here and it is noisy. However, it does back my belief that if you want the best yield and/or the fairest price then it is probably best to participate in the auction directly and avoid the middlemen.

Update:

I will probably end up breaking my "avoid the middlemen" rule this week in regards to my IRA. It has been sitting in cash sinceAugust 26, 2010.

It is my plan to buy the 30-Year TIPS with that money.

The yield on the 30-Year TIPS was 1.59% on the day I moved to cash. It is now about 1.9%. That's good enough for me. I may lock it in this week.

Over 30 years, that 0.3% difference adds up to about 9%. Assuming rates don't plummet before I buy, that cash has treated me quite well. :)

Jan. 13 (Bloomberg) -- The top U.S. commodities regulator approved today publishing a plan to curb speculation in raw materials including oil, gold and wheat as part of the most sweeping rewrite of Wall Street rules since the 1930s.

Right now Apple trades at around 17 times forecast earnings. If that rating stays about the same, then a market value of $900 billion would have to be supported by net income of about $53 billion.

Would $130 per man, woman, and child on this planet seem like a reasonable future valuation for Apple? Would $8 per year per man, woman, and child on this planet seem like a reasonable expectation for Apple's future profits?

The company has 40% gross profit margins. You may think that's ridiculous, but ours is not to reason why. People line up around the block to pay up. Individuals with a perfectly good iPhone will stand in line for six hours—updating their Facebook page—so they can be among the first in their town to own a new one. Customers are even happy to pay an extra $100 for an iPad with extra memory, even though they know the cost of that memory is maybe a dollar or two (if that). These people are not price-sensitive. They might be better described as price-immune.

People are nuts. I hope you realize that.

This might be your last chance to buy iStocks, iHomes, iCars, iPhones, and iPads before the face planting resumes. Get them now whilemoney is cheap.

Interest rates are starting to rise as the era of cheap debt comes to an end. If you can afford to borrow and put that money to good use -- say, on a home or car -- new debt may actually save you money.

This is your last chance to take on debt to save money.

Stocks should benefit as a natural inflation hedge, and they're coming off of the worst 10-year performance since the 1930s.

This is your last chance to buy stocks.

For consumers, there are plenty of other ways to take advantage of this interest rate shift before borrowing costs rise.

That will usher in a period of austerity as households and governments cut debt loads, slow borrowing and learn to live within their means.

This is your last chance to live beyond your means.

There's also a case to be made for using ultralow mortgage rates to buy a second home as a rental property.

This is your last chance to be a landlord.

I don't know about you, but the idea of driving around in an old, tired ride that costs a fortune to maintain and repair doesn't sound like fun.

This is your last chance to buy that new car.

Why does it suddenly feel like we're all moving to Detroit?

Detroit (AP) - Edwina Brown says she'll give the Detroit Public School system one more chance to improve before she decides to send her daughter to private school.

Detroit — Detroit Public Schools would close nearly half of its schools in the next two years, and increase high school class sizes to 62 by the following year, under a deficit-reduction plan filed with the state.

If PIIGS refers to nations that have overspent and are now overleveraging to pay for their deficits, the United States is feeding from the same trough.

It isn't quite the same trough. We import more than twice as much from the PIIGS as we export to them. That makes us some sort of Super Pig.

There has been huge talk about gold being in a bubble situation with a burst imminent, but perhaps palladium, silver and copper are better candidates for such an assessment.

If we're looking for speculative bubbles, would a stock that has quadrupled in a mere two years qualify? Take a look at the chart of global industrial stalwart Caterpillar (CAT).

If we compare GLD with CAT, gold looks like a model of stability. If there are any incipient bubbles in the market, Caterpillar and silver are much better candidates to experience a sudden pop than gold.

Must we choose?

Unwise was the wayfarer who journeyed by night, for in the shadows greedy eyes glittered...

If one looks back to the recent housing crisis, it is clear that the policy emphasis on easy money was one of the primary elements that created the illusory prosperity of the housing bubble and eventually led to crisis. The same is true of the various other crises that we have observed over the past decade. At present, I am convinced that the misguided policies that have been pursued in response to the recent downturn will again be reflected as significant new strains within a few years, if not sooner. While we will exercise as much latitude as possible to accept moderate investment exposures when the evidence is supportive, we have to be aware of the longer-term outcomes that are being set in motion by the present course of monetary and fiscal recklessness.

“If they bring a knife to the fight, we bring a gun,” Obama said in Philadelphia last night. “Because from what I understand, folks in Philly like a good brawl. I’ve seen Eagles fans.”

For the record, I'm not a fan of Republican Glenn Beck or Democrat Paul Krugman. I think both manage to create a climate of hate. I am not a fan of extremism.

It is my opinion that our country would be far better off with more moderates and lesspolarization.

It is one thing for political hacks like Olbermann or Beck or even the people at the Daily Kos to frame everything that happens in political terms and ignore pertinent facts. I expect that kind of behavior from them.

However, when a decorated academic economist does the same – and calls it careful analysis – I draw the line. I NEVER have seen or heard hateful rhetoric coming from other Nobel Prize winning economists, ever, and I have spent hours with many of them. Yet, with Paul Krugman, it seems that all we get is hate and name-calling and political talking points. I will let you be the judge of that kind of behavior.

"It is true that, in this era of downsizing and high prices, it can sometimes be difficult for a person to give unto Me 10 percent or more of their income, and still have enough left over for that new microwave or big-screen TV they've had their eye on," He said. "But do not forget that it is almost impossible for a rich man to enter the kingdom of God."

According to Raeburn, God currently has enough money saved to live comfortably throughout all eternity, but He may be forced to shutter a number of† under-performing religions.

Over the past five years the cost to U.S. Catholic dioceses of settling U.S. sex abuse cases involving priests has totaled nearly $2 billion, according to the Center for Applied Research in the Apostolate at Georgetown University in Washington.

Unfortunately, only two of those articles were fromThe Onion. Sorry about that. Here's a bonus article to make up the difference.

"We're stuck in the Dark Ages if we still believe some elaborately choreographed, archaic ritual has any impact on today's dynamic multinational corporations," New York University professor Nouriel Roubini said on CNBC this week. "If we really want Corporate America to restore our prosperity, then we have to own up to the facts, face reality, and kill every last one of our firstborn sons with our own bare hands."

I'm pretty sure that this last one is from The Onion anyway. Sometimes it is hard to tell.

...but Ford Motor Company (NYSE:F) is still viewed by many stock analysts as a strong contender with its story of profitability.

Here's achartof ford stock (and presumably its long-term story of profitability) over the years. It had 1970s pricing for a bit back in 2008 but have no fear. It can only go up from here apparently.

One of such investors Mr Mike Crowley, Director (Sales) for Ford Motors commended Nigeria for breaking new frontiers in partnership with foreign counterparts.

From what I hear, the Nigerian princes will even mingle with us lower peasants if given the opportunity.

In its third-quarter report, Sbarro noted that the company was "highly leveraged" and faced increasing commodity costs, particularly for cheese and flour. The company also pointed to a number of factors - its pressing large debt payments, low cash on hand, general economic uncertainty and no available means to restructure or refinance debt - that raised "substantial doubt regarding the company's ability to continue as a going concern."

Sbarro, which owns or franchises more than 1,000 fast-food Italian restaurants, is discussing restructuring its debt as well as potentially filing for bankruptcy, said the people, who asked not to be identified because the talks are private.

Barring serious deflation, these bonds are guaranteed to lose purchasing power for you if held until maturity. In the event of serious inflation, then expect to lose even more purchasing power as the inflationary gains are taxed.

Does it really take a huge leap of logic to think that there might be some commodity speculation going on right now, that maybe QE is responsible for it, and that maybe, just maybe, it can't actually save the world over the long-term?

{kind=link}