Click to enlarge.

Nice parabolic trend floor and failure.

December 17, 2015

2014 Monetary Policy Release

Based on its current assessment, the Committee judges that it can be patient in beginning to normalize the stance of monetary policy. The Committee sees this guidance as consistent with its previous statement that it likely will be appropriate to maintain the 0 to 1/4 percent target range for the federal funds rate for a considerable time following the end of its asset purchase program in October, especially if projected inflation continues to run below the Committee's 2 percent longer-run goal, and provided that longer-term inflation expectations remain well anchored.

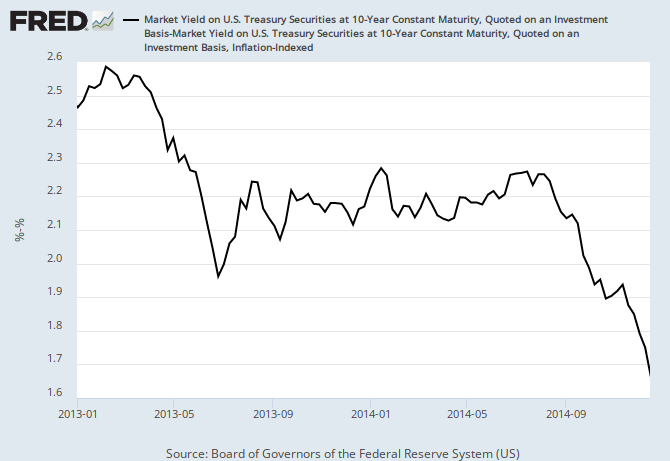

The next chart shows the 10-year inflation expectations as seen when subtracting the 10-year inflation protected treasury yield from the 10-year nominal treasury yield.

Click to enlarge.

The Fed might want to cut the deflationary anchor loose. We're in danger of being pulled under by it again, not that many seem to notice or care.

The Committee expects inflation to rise gradually toward 2 percent as the labor market improves further and the transitory effects of lower energy prices and other factors dissipate.

Good luck on that. I am at least 80% confident that the treasury market, as a whole, is smarter than a small group of relatively detached elitist policy makers meeting behind closed doors. Yeah, call me crazy if you must.

For what it is worth, and as a holder of long-term treasury bonds (with inflation protection), I also remain 80% confident that the Fed will not raise interest rates in 2015 and that the 30-year nominal treasury yield will not exceed 3% in 2015.

As a side note, I've said this before and it is worth repeating. My long-term treasury bonds have inflation protection for the same reason my house has fire insurance. I do not expect my house to burn over the long-term. I do not expect inflation to be a problem over the long-term. That said, I'm only 80% confident. The insurance is for the remaining 20% of the time. Further, I do not root for heavy inflation any more than I would root for my house to burn.

Those sitting in inflation protected treasuries actively rooting for high inflation clearly do not understand the situation. One does not get wealthier paying heavy taxes on heavy inflationary gains (each and every year). That's a path to the poor house. Of course, those without any inflation protection during such a period would be riding a bullet train to the poor house, so it's all relative I guess.

The financial policy of the welfare state requires that there be no way for the owners of wealth to protect themselves. - Alan Greenspan, 1966

Pick your poison. I've picked mine. This is not investment advice.

Source Data:

St. Louis Fed: Custom Chart #1

St. Louis Fed: Custom Chart #2

{kind=link}

8 comments:

Patient does not refer to time but to victim.

I think the 5/6 year treasuries are the sweetest part of the curve right now.

You should graph the 5-FF spread or the 5-1 spread.

Here's 5y-FF:

http://research.stlouisfed.org/fred2/graph/?g=UQ3

Here's 5y-1y

http://research.stlouisfed.org/fred2/graph/?g=UQ4

~0 seems like the right number

Actually, I guess the business cycle is a series of "parabolic trend failures" of that spread.

Rob Dawg,

Hilarious!!!

In a gallows humor sort of way, of course.

http://exurbannation.blogspot.com/2014/12/mortgage-rate-v-10-year-rate-spread.html

CP,

The most amusing part of the curve, at least to me, is this one.

30-year minus Fed Funds

Most expected the spread to contract as the fed hiked rates. They are trying to make sense of it right now. Shakes their world view a bit.

Some expected the spread to contract if the fed didn't hike rates, and even more if they did.

I am in the latter camp, for what it is worth.

Rob Dawg,

It is always important to be mindful of the GAP.

Post a Comment