Click to enlarge.

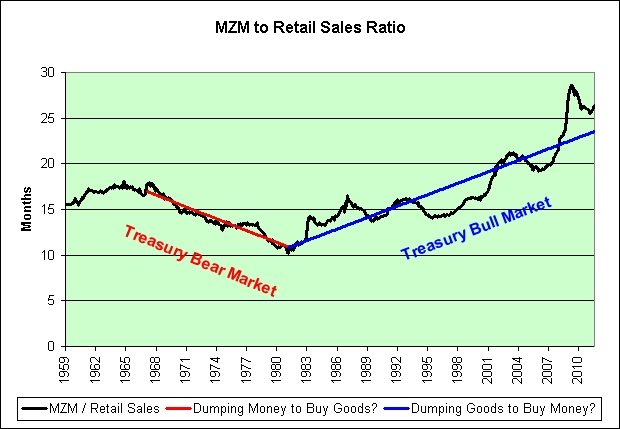

There's a lot that could be said about this chart. Rising income inequality? China dumping their goods on us for our money? The tanking real estate market? Our credit bubble? Financial repression?

I don't think the treasury bull market will last forever, but predicting its demise has been a bit tricky to say the least. Never a better time to short treasuries? Oops.

I was rather indifferent personally. I thought real yields would continue to fall and they have (just like the 1970s). I had little opinion on nominal yields though. 1970s? Japan? You tell me and we'll both know.

Those buying and holding today's 10-year 0.0% TIPS will lose purchasing power after taxes. If the bull market continues it sure won't feel like it.

That said, take a look at global short-term real yields as seen in the chart in the following link though. You could potentially do worse.

June 2011

A New Era of Global Financial Repression

A look at average real short-term policy rates over the past 15 years shows how extraordinary the current environment is (see Chart 1). By this metric, the entire world is, on average, running a very repressive interest rate policy. Even the majority of emerging market countries are holding rates abnormally low compared with inflation and growth trajectories.

I'm about out of "safe" advice for the constitutional saving peasants. We're being oppressed. The central banks of the world are desperately attempting to get us to embrace risk at exponentially increasing levels. My idea of risk taking was buying long-term TIPS, I-Bonds, canned goods, and toilet paper on the hopes I would do it before others did. I'm not exactly sure that's what our superiors had in mind.

Source Data:

St. Louis Fed: Retail and Food Services Sales

St. Louis Fed: Retail Sales (Discontinued Series)

St. Louis Fed: MZM

12 comments:

I found the implications of this population graph interesting.

In 2020 the baby boom echo is going to be entering their 30s. They're going to be tired of being held down by conditions.

There looks to be a sizable echo echo forming, too.

Plus the boom itself is steps away from Medicare.

Poor Generation Y is going to get pulled in 2 directions.

I think if the PTB let another debt bubble rip they can get our debt to GDP up to Japan and the UK's -- 4X or so. We're still pikers down at 3.5:

http://research.stlouisfed.org/fred2/graph/?g=21d

We're not necessarily Japan, things can actually get cyclical here again.

Dunno how, but if they can do it, they will.

Troy,

We're not necessarily Japan, things can actually get cyclical here again.

Dunno how, but if they can do it, they will.

I'm picturing riding that wave between unbearably high 0.25% Fed monetary policy and 0.00% super easy Fed monetary policy.

We can get there. We just need a LOT more leverage, lol. Sigh. I say this somewhat tongue-in-cheek of course.

September 6, 2007

Let Them Eat Cake!

In 2000, then-BOJ Governor Masaru Hayami was widely derided for raising rates from zero to 0.25 percent. Pundits called him Japan's answer to Herbert Hoover. Yet Hayami was trying to force Japan Inc. to implement structural reforms. It didn't work and rates returned to zero in March 2001.

Japan has 2% mortgage rates, so that's probably coming to help Generation Y afford to buy.

I wonder if the system will preserve the current tax rates or revert to Clinton-level rates, for the $100,000 income level Clinton takes $5000 more.

I guess the Fed could print the money we need to redeem SSA's bonds, that would balance the deflationary effect of the higher tax bite.

Rates might remain low even as 4-5% inflation returns.

That doesn't make any sense but neither does sustained $1.3T+ deficits.

Troy,

Rates might remain low even as 4-5% inflation returns.

That doesn't make any sense but neither does sustained $1.3T+ deficits.

It could make sense if we fought World War 2 again using economists instead of soldiers. Sigh.

August 3, 2011

Charting the War on Savers

Hey Mark,

since I am never as smart as I imagine myself to be, could you review why a TIPS fund is a bad idea...VIPSX. I have a Roth 401k that must be in a fund (Vanguard)...and I looking for some shelter. Many thanks.

fried,

VIPSX has a -0.32% real yield, an average maturity of 9.5 years, and annual fees of 0.22%.

If you bought a 9.5 year TIPS bond with a -0.32% real yield then I could pretty much tell you today how you would be doing 9.5 years from now. I'd expect you to lose 3% of your purchasing power.

The fund would lose an additional 2% due to the annual fees. That's one reason I prefer to avoid funds (but you have no choice in that).

Is losing a virtually guaranteed 5% over the next 9.5 years better than your alternatives? It is sad that we even have to think this way. It could very well be (especially if the other fund choices have higher fees and the economy continues to stagnate).

There's more though, and I think this is the important part.

A 9.5 year TIPS individual bond you buy today will mature in 9.5 years. If you hold it until maturity then you really don't care all that much what interest rates do. You might even hope that they rise so that when the bond matures you'll have some place to reinvest.

A 9.5 year TIPS bond fund will not mature in 9.5 years. 9.5 years from now you'll still own a 9.5 year TIPS bond fund. If you want your money back at that time then you must sell it to someone else. There is risk in that because you do not know what they would be willing to pay you for it.

Here's a worst case scenario.

You own the fund for 9.5 years and lose 5% of your purchasing power (interest rates remain unchanged). Just before you decide to cash out though, interest rates spike way higher. So you've locked in that 5% loss AND the fund's price crashes too (due to rising real interest rates). Ouch.

Of course, this same process can also work in your favor if real interest rates continue to fall.

I would also point out that stock funds also share this same behavior (to an even higher degree). Individual stocks never mature. You are very dependent upon others to give you a good price when you wish to sell.

Hope this helps. There aren't many easy answers for those valuing safety in this environment.

"There aren't many easy answers for those valuing safety in this environment."

Easy answer #1:

Safe. The locking, fire-proof, cemented to the floor kind.

Anonymous,

Easy answer #1:

Safe. The locking, fire-proof, cemented to the floor kind.

I bought that very thing when I turned bearish in 2004. No joke!

It is bolted to the cement floor.

Easy answer #2:

Something with a safety in a safe! ;)

Mark,

many thanks for the analysis. I did a much rougher calc and came to the same dismal conclusions. I may see if I can roll this sucker over to a bank.

If not, then it will be an expensive lesson. I'll post whatever the outcome is, just in case anyone else is in the same swamp.

Again,my thanks.

fried,

Bull Market: Really high tide, 'laws of physics' free stranded sailboat: A local man was breathing easier Wednesday after unusual high tides - plus lines and pulleys, inflatable floats, a Ford Explorer and a small tugboat - freed his 84,000-pound sailboat from the shallows of Lake Hillsmere.

Bear Market: USS Regulus (AF-57): After three weeks of attempting to refloat Regulus, it was finally decided that the damage she had incurred was too severe to warrant salvage.

Sigh.

Mark,

I'd prefer to re-fight the Civil War with economists, rather than WW2. Much higher casualty rates. Why, if we were lucky we could get the economists to reprise the cornfield at Antietam.

Who Struck John,

Yes. Your plan sounds superior. Let's be sure to offer a public service announcement *after* the economic war is over, lol.

You might be the toughest economist on your block, but you cannot win a fight with a Parrott Rifle.

Post a Comment