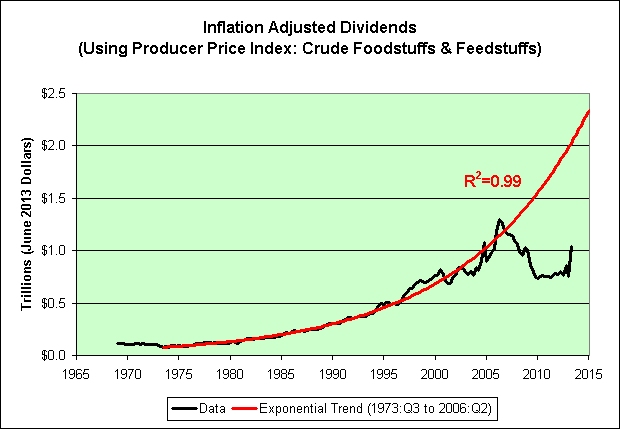

Click to enlarge.

Click to enlarge.

Real estate tops the list at #1. I'm sure we'll bounce back someday. Just need to keep pushing this asset higher and higher so that people can finally sell the darned things again (the mortgage liability is not included in the asset chart for somewhat obvious reasons). And as an added bonus, the higher we can push this asset price the higher we can get those property taxes. Everybody wins!

Pension fund reserves come in at #2. Other than

record pension underfunding even as the stock market has risen 160% from the bottom in 2009, what could possibly go wrong with that asset class?

Corporate equities come in at #3. It's nice to see them

doing so well lately. It does make me wonder though. The people who warn me about the treasury bond bubble also tend to be the ones who tell me that the retail investor hasn't gotten back into the stock market yet. It's very confusing to me because it looks like about 60% of the stock market value is sitting right there in the hands of the retail investor. Very odd.

Deposits come in at #4. Don't forget to load up on the

0.5% 5-year CDs. They might not yield nearly as much as

their treasury equivalents, but they are still a bargain at any price. Has anyone ever warned of a certificate of deposit bubble? I think not. Perhaps it is because CDs are held to maturity by default but it takes maturity to hold a treasury to maturity. Just a theory. Of course, if you aren't much of a risk taker then you can pick something with a shorter maturity. You'll have to sacrifice some of that juicy yield though! Mwuhahaha! Sorry, there I go being immature again.

Equity in noncorporate business comes in at #5. I've got to tell you. That takes guts. It's a tough world out there. Could strike it rich. Could be stomped by big business. At least the Great Recession II can't happen. The Fed has permanently put a stop to recessions. I can't personally prove it, but if everyone believes it then it must be true. Only rising rates can cause a recession. Therefore, ZIRP makes recessions impossible. Just because

we're very deep into uncharted territory, doesn't mean that investors don't understand exactly how the future will play out. It's self-evident, especially when CNBC repeatedly tells us just how self-evident it is.

Mutual funds come in at #6. There are some bonds in there, but my guess is that the majority is stocks. That would be even more exposure to the equity markets for the retail investor (who I am continually told is missing out on the rally). Mutual funds are the safer way to go of course, because nobody wants to risk a 20% loss all at once when that same 20% loss can be locked in and guaranteed over 20 years (assuming 1% per year in fees). Whatever you do, do not underestimate the power of a "professional" active fund manager to add value just because

76% fail miserably when trying to outperform the market index.

Durable goods come in at #7. That's my favorite! As I've mentioned in the comments recently, the United States dominates the self-storage industry with

"almost 90% of the global market". Don't let that deter you from buying even more durable goods to protect your wealth though. One place near me only charges $696 per year for a 5'x5' unit. That's a screaming bargain for someone with too many plastic coat hangars. Paying someone to store them for you is

money well spent. Somebody needs to fund the CEO's

$3.23 million salary. Do you have any idea how hard it is to manage other people's

money stuff? Not just anyone can point a person towards their stuff without actually wanting to do inappropriate things with that stuff when they aren't around. It takes serious discipline. If only the

banking system could do the same!

At #8 we've got corporate bonds. They can't ever seem to offer enough to satiate our appetites. I'm especially interested in chasing the yields of the non-investment grade bonds. What's

the worst that could happen again?

We're to #9. Finally some safety! Yes, sir. As long as each municipality has its own working monetary printing press (in sharp contrast to Detroit's broken one) and we can work through the serious injuries of the dotcom and housing bubbles, then you'll no doubt sleep very well holding tax-free municipal bonds to maturity and/or racing towards the sell button on your trading platform of choice someday.

And lastly, we've reached #10. It's funny that so much time is spent warning us about a treasury bubble when individually purchased treasury bonds make up such a tiny amount of our personal assets (less than 2%). In my experience, very few people even know how to buy them directly from the government. I'm not judging. I've seen many hours of financial TV in my life and I've never seen anyone offer advice on how to buy a treasury bond. I don't recall the term I-Bond ever coming up either. It's almost like there's no money in it for them if bonds are purchased directly from the government.

This is not investment advice!

Source Data:

FRB: Z.1 Release